Reserve bank of australia

Australia's surcharge rules are changing.

Here's what that means for our software platforms and merchants.

Updated on 12 June 2026

The Reserve Bank of Australia (RBA) has finalised reforms to card payment surcharging and interchange fees, effective 1 October 2026. As your payments partner, we're committed to making this transition straightforward for your business.

We are currently in the planning and preparation phase, working closely across teams to ensure everything is in place for a smooth transition for our partners and customers.

What has the RBA decided?

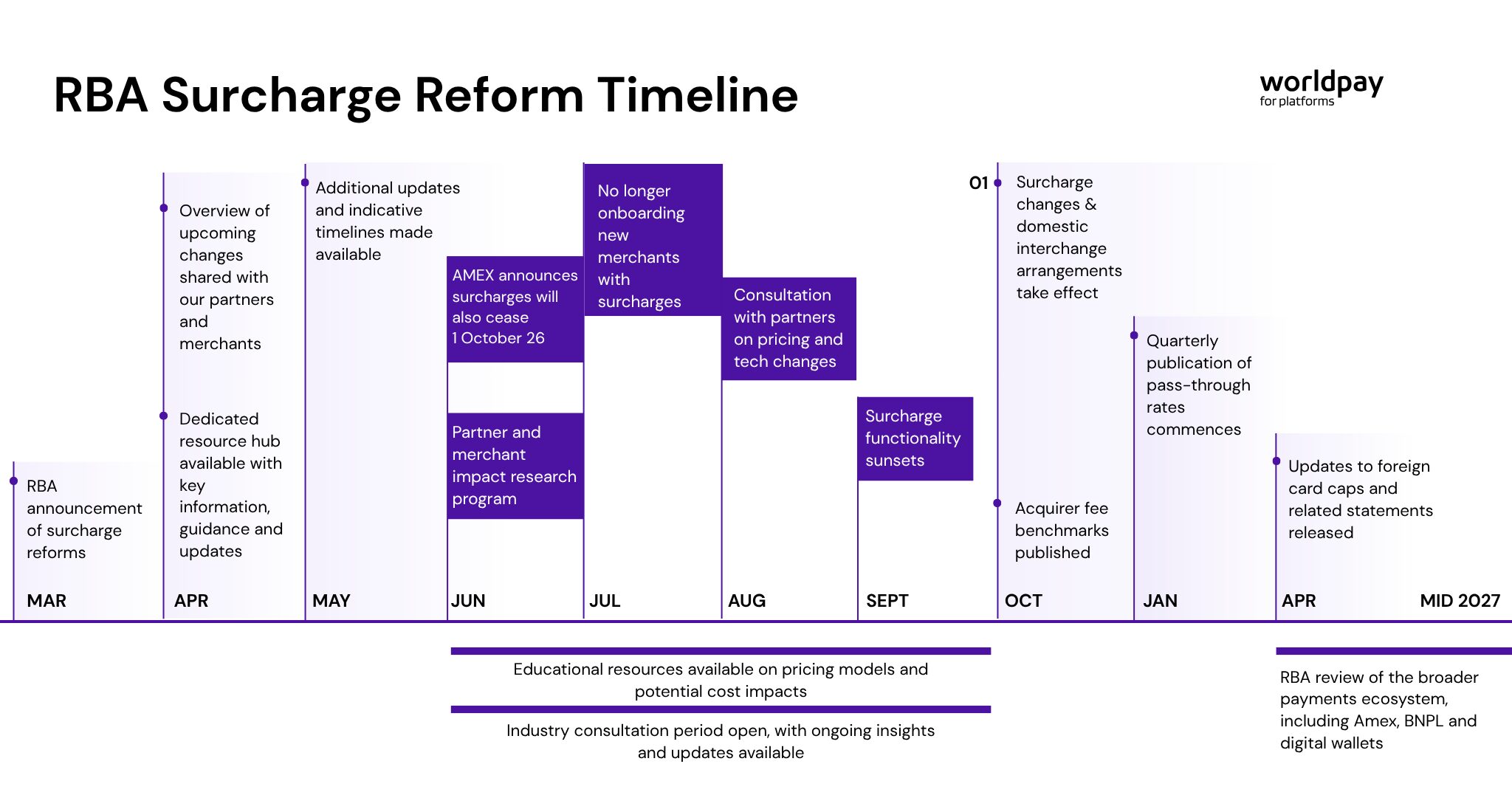

On 31 March 2026, the RBA released its final Conclusions Paper on Merchant Card Payment Costs and Surcharging.

The key decisions are:

- From 1 October 2026, merchants will no longer be permitted to apply surcharges on Visa, Mastercard and eftpos card payments, following the RBA’s removal of restrictions on scheme no-surcharge rules.

- Consumer credit card interchange will change from 1 October 2026. We will assess any impacts to our pricing arrangements and communicate any changes applicable changes separately.

Key dates shared by the RBA

| 01 October 2026 | Surcharge ban + domestic interchange changes |

| 30 October 2026 | Acquirer fee benchmarks published publicly |

| January 2027 | Pass-through rates published quarterly |

| 01 April 2027 | Foreign card cap + enhanced merchant statements |

| Mid- 2027 | New RBA review: BNPL, wallets |

American Express surcharge update

In early June, American Express (AMEX) has also announced that surcharging will no longer be permitted on AMEX card payments in Australia from 1 October 2026.

This is a separate change from the RBA regulations relating to Visa, Mastercard and eftpos and aligns the treatment of American Express with other major card networks

The change applies specifically to AMEX card surcharging and does not change how payment processing fees are applied.

What this means for your business?

If you currently surcharge

If you don't currently surcharge

If you're a software platform

What merchants need to know about the changes

One of the most common questions we're hearing is whether payment fees are disappearing.

The answer is no.

From 1 October 2026, businesses will no longer be permitted to apply a surcharge to Visa, Mastercard, eftpos and American Express (Amex) card payments. However, businesses will generally continue to incur payment processing costs when customers pay by card.

Payment fees aren't disappearing. The key change is that businesses can no longer recover these costs through a separate card surcharge.

Want to learn more?

Read our practical guide explaining what is changing, how to determine whether your business may be affected, and what steps you can take to prepare.

What this looks like in practice for merchants

| Today (Before 1 October 2026) | After changes (From 1 October 2026) |

| Businesses can apply a surcharge to card payments | Surcharges on Visa, Mastercard, eftpos and Amex card payments are no longer permitted in Australia from 1 October 2026 |

| Payment processing fees apply when accepting cards | Payment processing fees still apply when accepting cards |

| Customers may see an extra charge at checkout | No separate surcharge can be added at checkout |

| Businesses may use surcharging to offset payment costs | Businesses will need to consider how costs are managed within their overall pricing model |

| Ancillary fees such as dishonour and admin fees can be passed on to customers | There are no changes to these fees under the reform, the reform affects transaction surcharges only |

Questions businesses are asking

Do payment fees disappear?

Does this affect direct debit payments from bank accounts?

Does this affect both one off and recurring payments?

Does this affect American Express (Amex) payments?

How do I know if I currently apply a surcharge?

How much surcharge income does my business currently receive?

Do I need to increase my prices?

Do I need to do anything right now?

What happens next, and how we will support you

We are taking a phased approach to ensure we can carefully plan and prepare while supporting merchants and platform partners through each stage of the transition.

Here is what you can expect from us:

- To prepare our partners for the change, we will no longer be onboarding new surcharged merchants from 1 July 2026.

- Throughout August, we will communicate directly with partners on any changes that may impact them, including changing, when and any actions required.

- We will then notify all affected merchants directly, or through software partners, with personalised guidance on what needs to change and by when.

- We are planning platform updates to remove card surcharging functionality ahead of the 1 October 2026 deadline. We will proactively review our merchant service fee rates to ensure they reflect any cost reductions that we gain and pass savings through to our partners.

- Nothing changes immediately. Our phased approach towards the 1 October 2026 deadline, will give you time to prepare, and we will support you every step of the way.

- Our team will be available to answer your questions and walk through any implications for your business. If you have further questions before then, please contact us here

Your next steps

We are committed to making this transition as seamless as possible for every merchant and platform partner.

To help you prepare, we recommend the following:

- Review whether you currently apply a card payment surcharge.

- Check if your payment plan is fee-free or relies on auto-surcharging.

- Watch for a direct communication from us with personalised guidance.

- Publicly available industry information may help businesses understand broader market changes. However, individual pricing outcomes vary based on business characteristics and commercial arrangements.

- Contact us if you have questions, we are ready to help.

Alison Morris

General Manager, International Integrated and PlatformsHelpful resources

Have further questions?

Our team will be available to answer any questions and walk through the implications for your specific business. If you have further questions before then, please contact us.